As the year draws to a close, many priorities come into focus for wealth managers. This is the season when firms close their books, review portfolios, and ensure clients are positioned to maximize tax value as they head into the new year. A key source of adding tax value for clients is tax loss harvesting.

While most advisors understand the value of tax-loss harvesting, as we enter the fourth quarter, it is a timely moment for teams to revisit the process and confirm that they have the proper steps in place to help optimize a client's after-tax outcomes.

This paper serves as a practical primer. It offers a framework to help advisors position themselves for success in the final quarter, deliver meaningful after-tax outcomes for clients, and approach harvesting with structure rather than ad hoc execution. We also highlight key considerations to carry forward as practices close the book on 2025 and prepare for 2026.

The Value of Tax-Loss Harvesting

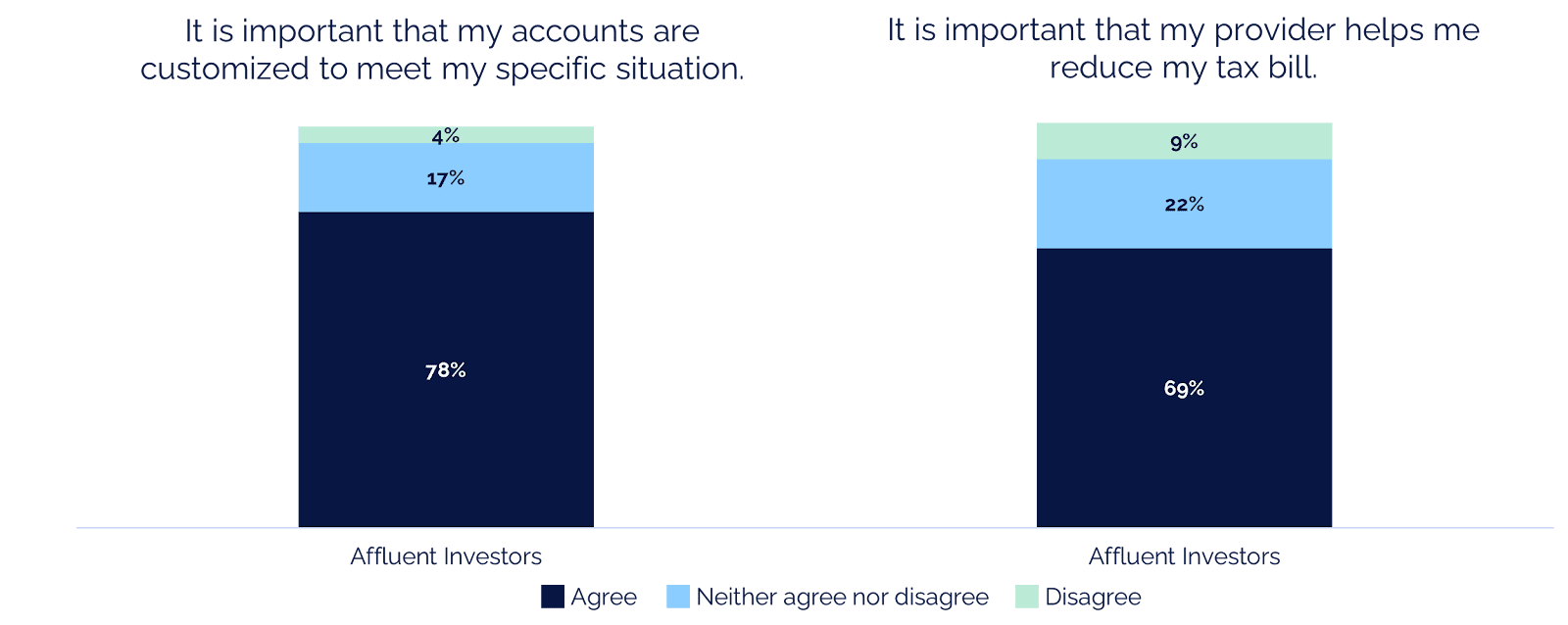

Investors are also placing more emphasis on tax management in wealth planning. A Cerulli survey of affluent investors found that 78% value account customization and 69% want providers to help reduce their tax burden (Figure 1). One of the most valuable ways a wealth manager can reduce an investor’s tax bill is tax loss harvesting.

The concept of tax-loss harvesting is straightforward: realize capital losses, use them to offset gains and ordinary income, and lower the client’s tax bill. For the right investors, these savings can boost after-tax returns, often referred to as “tax alpha.” The value of tax alpha varies by investor, with higher tax rates and greater capital gains burdens leading to larger benefits.

Figure 1: Affluent Investors: Importance of Account Customization and Tax Reduction, 2024

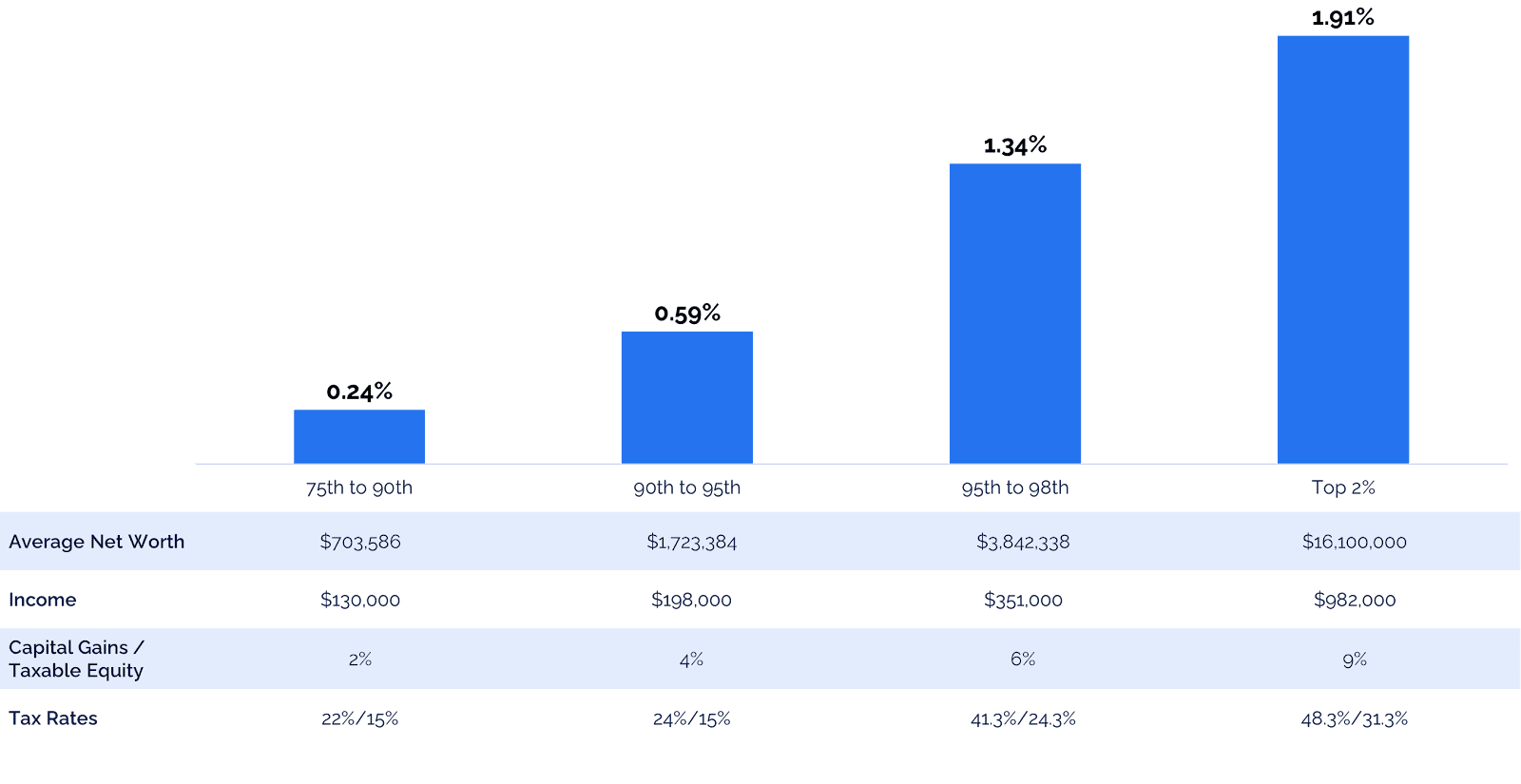

Research by Kevin Khang, Joel Dickson, and Thomas Paradise (2021) indicates that wealthier investors reap the most significant benefits from loss harvesting. In their study analysis, investors in the 90th to 95th wealth percentile achieved an annual tax alpha of 0.59%, while investors in the top 2 percent reached 1.91% (Figure 2).

Figure 2: Annual TLH Alpha with Realistic Assumptions about Investors

Source: Khang, K., Paradise, T., & Dickson, J. (2021). Tax-Loss Harvesting: An Individual Investor’s Perspective. Financial Analysts Journal, 77(4), 128–150. https://doi.org/10.1080/0015198X.2021.1963187

This material may contain forward-looking information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. Tax rates for each investor profile are listed in the bottom line of the table and include federal, state tax and NIIT where applicable. There is no guarantee that any of these views will come to pass.

Not all tax-loss harvesting is created equal

The value of tax-loss harvesting depends heavily on the quality of the process. Several factors influence the realized tax alpha, including how often portfolios are reviewed, the granularity of portfolio holdings, the level of cash flow, and whether tax savings are reinvested. While not all of these are within an advisor’s control, both the frequency of portfolio checks and the granularity of portfolio building blocks can be directly managed.

Frequency of portfolio checks

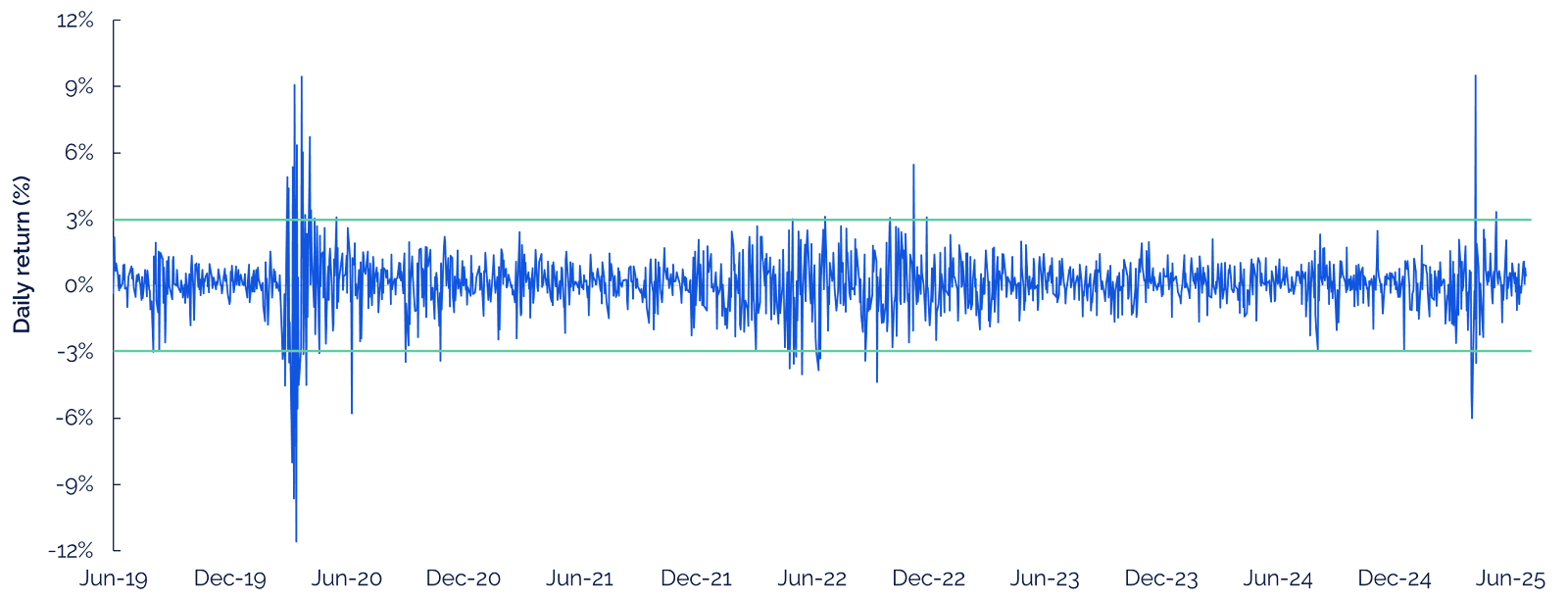

Market volatility does not follow a calendar, underscoring the importance of regular portfolio reviews. An analysis of daily returns for the iShares S&P 500 ETF from June 2019 to June 2025 illustrates this concept (Figure 3).

Figure 3: S&P 500 Index Daily Price Returns (June 2019 – June 2025)

From June 2019 to June 2025, only 3% of trading days had a portfolio move greater than 3% and only 9% of these days occurred in the final quarter of the year.

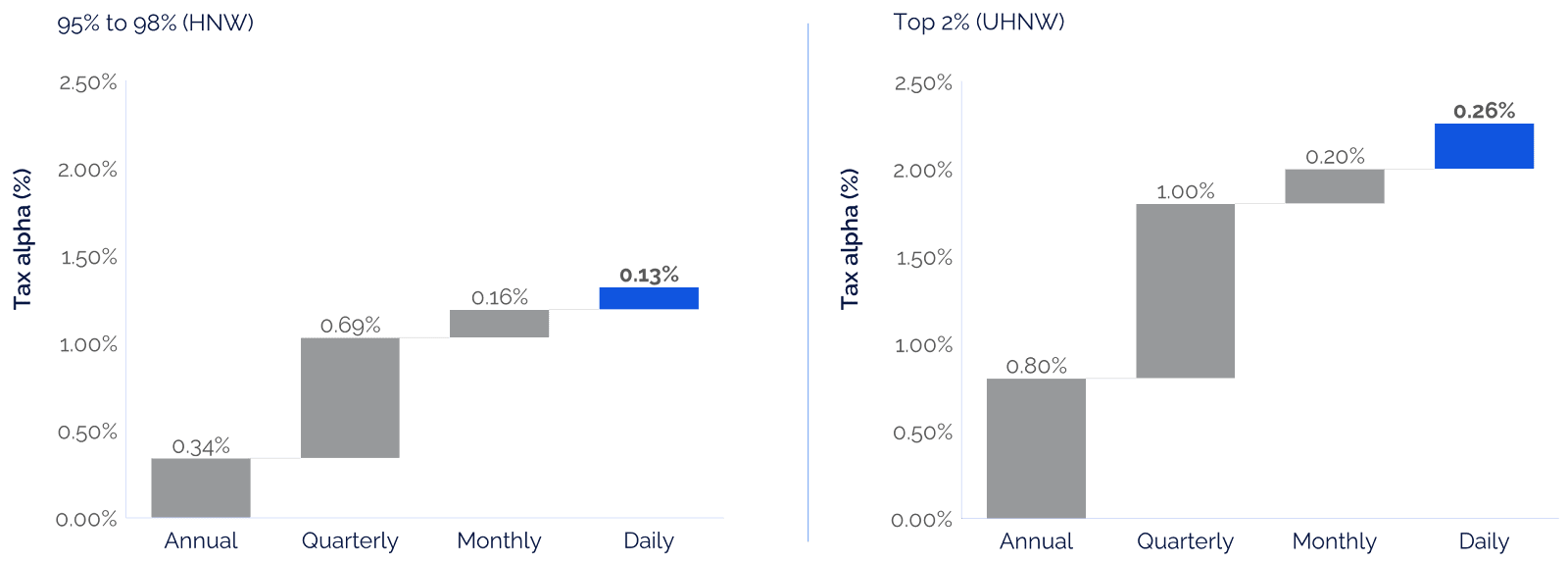

Advisors who limit portfolio checks to year-end leave a substantial amount of loss harvesting value on the table. For a high-net-worth client, the difference in tax alpha between annual and daily portfolio checks was just under 1%. For an ultra-high net worth client, the amount of tax alpha missed is over 1.1% (Figure 4).

Figure 4: Average 10-year TLH alpha by harvest frequency

Granularity of portfolio building blocks

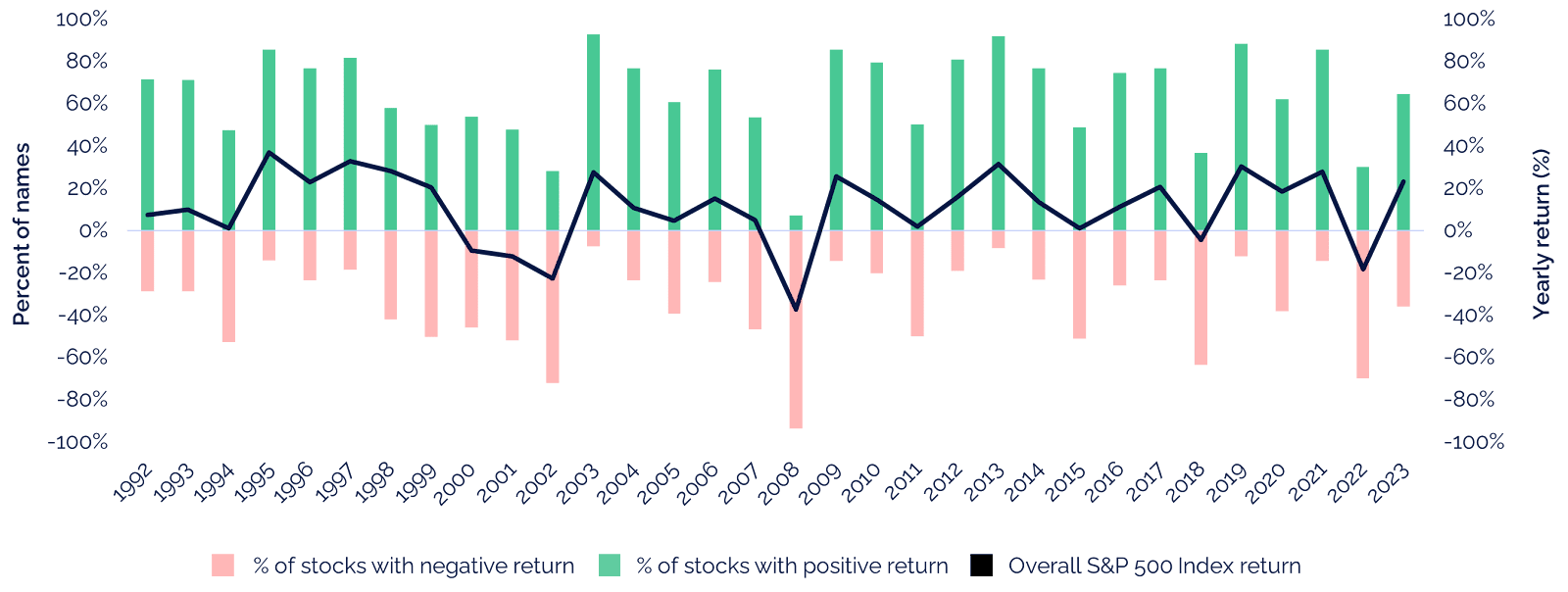

Tax-loss harvesting depends on securities trading below their cost basis, and greater portfolio granularity increases these opportunities. An analysis of individual stock returns within the S&P 500 Index illustrates this point (Figure 5).

Figure 5: Percent of stocks in the S&P 500 Index with a positive and negative return, versus the overall S&P 500 Return (1992-2023)

Source: Vanguard, “What is direct indexing?” Accessed October 2, 2025.

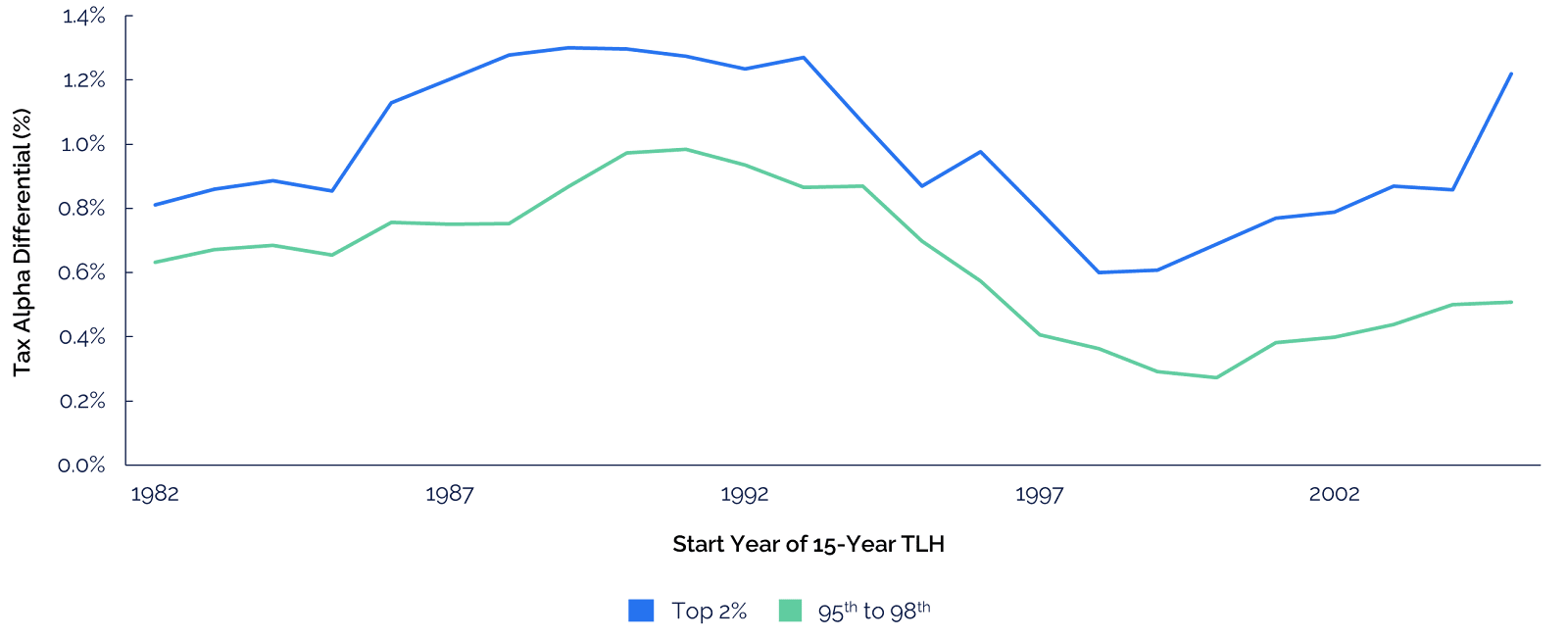

While the index may rise overall, its components move differently. An investor holding an ETF that tracks the index cannot harvest losses if the ETF has appreciated, but an investor holding the underlying individual stocks can sell those that have declined. This flexibility allows portfolios that hold individual securities to potentially capture more losses and generate higher tax alpha (Figure 6). There are many factors that influence after-tax returns and tax alpha among vehicle types, including but not limited to, factors involving 1) the specific client, such as cash flows, capital gain profile, tax rates, holding period, and liquidation plan, 2) the market environment, including direction, volatility and dispersion, and 3) the investment strategy, such as the number of holdings, anticipated portfolio turnover, and holding correlations.

Figure 6: TLH Alpha Differential (Direct Indexing – Index Fund) by Return Environment

Who can benefit the most from tax loss harvesting

The benefits of tax-loss harvesting vary by client and depend on tax profile, portfolio composition, income mix, and time horizon. Advisors can look for several markers to identify where the opportunity is greatest.

High-tax-rate investors

Clients in the top federal and state brackets tend to benefit the most from tax loss harvesting. Their higher effective tax rates translate directly into greater value from offsetting gains and reinvesting savings.

Clients with recurring capital gains

Investors who regularly realize gains through business sales, real estate transactions, or alternative investments are especially strong candidates. Absent these gains, harvesting produces limited benefit beyond the $3,000 ordinary income offset.

Investors with steady contributions

Clients who consistently add to portfolios create new lots with higher cost bases, which refreshes future harvesting opportunities.

What advisors should consider as they begin loss harvesting season

Advisory practices managing taxable portfolios can take several steps now to prepare for loss-harvesting season. The priority is to establish clear processes and structures that enable teams to identify opportunities effectively and create value for clients.

Get tax-lot visibility

Tax lots are the foundation of harvesting. Without clean, accurate data, advisors risk missing opportunities or inadvertently realizing gains instead of losses.

Thorough Approach: Use tax-loss harvesting software or partner with a specialist subadvisor to consume custodian lot-level data in real time. This ensures every opportunity is surfaced and no cost basis adjustments are missed.

Streamlined approach: Monitor gains and losses directly within your custodian platform or advisor tech stack. Set a calendar cadence or create preset views that allow you to identify lots trading at a loss quickly.

Match opportunities to client profiles

Client tax sensitivity drives more than half of the potential value from harvesting. Misalignment wastes effort on clients who derive little benefit, while overlooking those who stand to gain the most.

Thorough Approach: Collect and maintain detailed client data on tax rates, realized gains, and capital gains budgets in a centralized system. This allows you to match harvesting opportunities with client-specific tax sensitivity precisely.

Streamlined Approach: Segment clients into tiers (e.g., high, medium, low tax sensitivity) based on simple heuristics like tax rate or known gains exposure. Focus harvesting efforts on the highest-value segments.

Be ready for volatility

Opportunities for tax-loss harvesting are unpredictable and often occur outside standard harvesting windows. Advisors who are prepared to act during periods of volatility are best positioned to capture losses and maximize value.

Thorough Approach: Use daily monitoring tools or partner with a subadvisor who reviews portfolios each day and can execute immediately when markets move. This is especially important since volatility often clusters, creating multiple harvest windows in short succession.

Streamlined approach: Establish alerts or a weekly monitoring routine to catch drawdowns. This may miss some opportunities, but it still provides more opportunities than a December-only review.

Decide how to trade

Deciding whether to harvest a position has meaningful implications for both realized tax savings and portfolio integrity. Advisors should apply a structured framework that balances tax benefits with investment discipline. Such a framework should weigh the potential tax savings against the investment risk and long-term strategy, ensuring that harvesting decisions improve after-tax outcomes without undermining portfolio objectives.

Thorough Approach: Apply a risk-based approach that incorporates factor exposures, tracking error, and other measures of portfolio risk to minimize unintended portfolio drift while maximizing realized losses.

Streamlined Approach: Use position-weight guardrails (e.g., harvest when a position drifts more than 50 bps from target). This is simple to implement but can create unintended portfolio consequences, introducing more tracking error.

Manage wash-sale risk

Wash sales can entirely negate a harvest and even strand capital losses in non-taxable accounts, eliminating their future value. Avoiding them protects both clients and the advisor's credibility.

Thorough Approach: Integrate household-level trade history across qualified and non-qualified accounts, with automated checks before executing any harvest. Subadvisors typically provide this functionality.

Streamlined Approach: Implement a 31-day trading lockout around harvesting activity to prevent inadvertent wash sales. While less precise, it is effective in reducing disallowed losses.

What advisors should consider as they begin loss harvesting season

As you prepare for the new year, three questions are worth asking inside your practice:

1. How tax-sensitive are our clients?

Not every household needs a robust tax management program. Segmenting clients by tax rate, expected capital gains, and contribution patterns will help you decide how much time and infrastructure to invest.

2. Do we have the systems and data to act quickly?

Daily monitoring of lots, client-level tax budgets, and household-level wash sale checks is increasingly the standard. If your practice cannot support this internally, consider adding technology or partnering with a sub-advisor.

3. How do we balance taxes with portfolio design?

For firms deeply committed to manager selection and risk budgeting, protecting portfolio integrity matters just as much as generating tax savings. Clear rules for weighing investment risk against tax benefits ensure the “tax tail does not wag the investment dog”.

Advisors have access to a wide range of technology platforms and sub-advisors, each offering strengths in different strategies. There is no single correct model. The key is for firms to determine which approach aligns best with their clients, their practice, and their overall philosophy.

Robust tax management is a year-round process

Taxes are an unavoidable part of investing and a clear area where advisors can provide measurable value. Increasingly, clients also expect their advisors to play an active role in managing their tax burden.

Tax-loss harvesting is not about timing the market or chasing a quick win. It is about putting structure around volatility, capturing opportunities when they arise, and ensuring that more of your clients’ capital stays invested and compounding.

- As year-end approaches, now is the time for firms to:

- Review tax-lot data and ensure accuracy.

- Identify the clients who are most likely to benefit.

- Put processes in place to monitor volatility and act quickly.

- Define how you will weigh tax savings against portfolio risk.

Looking beyond December, the most effective tax loss harvesting programs start on January 1. By committing to a systematic, year-round approach, you can move from opportunistic harvesting to a consistent, differentiated service that clients will value.

The opportunity is clear: proactive tax management is one of the most direct ways to show clients the after-tax value of your advice.

Disclosures

Quorus Inc. (“Quorus”) is an advisor registered in the states of Connecticut and Pennsylvania. The material presented is for informational purposes only and should not be construed as investment advice. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular security, strategy, or investment product. Investing in securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes and may not reflect actual future performance. Product images shown are for informational and illustrative purposes only, and may not reflect how they will actually appear within the product. Nothing in these materials should be construed as personalized investment advice, which can only be provided in one-on-one communications.

Investing entails risks and there can be no assurance that any investment will achieve profits or avoid incurring losses.

This material is intended solely for educational purposes and should not be construed as investment advice, a recommendation, or an offer or solicitation to purchase or sell any securities. The opinions expressed are as of the date(s) indicated and are subject to change without notice. Reliance upon the information herein is at the sole discretion of the reader.

Figure 6: We used the top 400 securities by market capitalization contained in the Axioma US4 (AXUS4) risk model to create a capitalization-weighted index portfolio (Axioma 400), which is similar to an S&P 500 Index or Russell 1000 Index portfolio. This index is reconstituted on the first day of each calendar year, using market capitalizations as of the last day of the prior year. All analysis in the article is based on the individual constituents of this index. We used the daily returns of the Axioma 400 constituents from the beginning of 1982 to the end of 2019. This roughly 40-year period encompasses diverse return environments, including the 1990s (known for the Great Moderation and sometimes called the Roaring Nineties), the dot-com bubble and bust in the early 2000s, the 2008–09 global financial crisis, and the subsequent decade driven by highly accommodative monetary policies.

The TLH algorithm maintains individual tax lot holdings of all positions, updating them with associated returns daily. To initiate loss harvesting, a loss threshold of 10% relative to the cost basis is applied; 10% strikes a balance between harvesting when losses are material enough and an economic use of turnover and tracking error.

Consistent with the literature (e.g., Dickson et al. 2000; Berkin and Ye 2003), our algorithm prioritizes the tax lots with the greatest loss per share using HIFO (highest in, first out) accounting when harvesting losses. Cumulative loss harvests are used at the end of each calendar year to offset any capital gains assumed to be available; the algorithm keeps track of short- and long-term capital losses and offsets the capital gains of the same character before applying any unused losses to other net capital gains. The algorithm takes the harvest tax rate and the liquidation tax rate as exogenous parameters. As mentioned earlier, the algorithm then mechanically applies TLH by offsetting any LOI with the harvest tax rate and liquidates the specified portion (between 0 and 1) at the end of the investment horizon with the liquidation tax rate. Any resulting tax savings are reinvested into the portfolio at the end of the calendar year. Unused losses are carried forward to the subsequent calendar year, retaining their character (i.e., short term or long term) for use in future periods. Dividends received are assumed to remain in a separate cash account and are reinvested at the end of each quarter along with any predefined cash flows. Securities that received dividends are held for a minimum of 61 days to ensure that the dividends receive qualified status; accordingly, these securities cannot be sold for loss harvesting during this period.

When a security is sold for loss harvesting, we assume that there is an identical replacement security to navigate the wash-sale rule. We further assume that the replacement security cannot be sold for another loss realization until 31 days have passed from the initial harvest date. At the end of the investment horizon, we compute the TLH alpha—defined as the difference in annual internal rate of return (IRR) between the baseline portfolio without tax-loss harvesting and the portfolio with TLH—after netting out the final tax liability from liquidation; if the liquidation is partial, tax lots with the smallest capital gains per share are sold first. Trading costs of 25 bps (Corwin and Schultz 2012; Chaudhuri et al. 2020) and 10 bps are applied for trading individual securities and commingled investment vehicles, respectively.

For each investor profile, we launched a 15-year TLH strategy every January from 1982 to 2005.

In search of an alternative method of tax-loss harvesting, we repeated the previous analysis of TLH alpha dispersion by return environment with one difference: instead of using individual securities in the portfolio, we deployed TLH with a commingled investment vehicle. Specifically, we constructed an index portfolio based on the Axioma 400 and pursued TLH with this portfolio. The investor in this setup, through the index portfolio, has the same exposure to the Axioma 400 index as the direct indexing investor. What separates the index portfolio investor is that she can no longer exploit cross-sectional volatility and has to rely solely on time-series volatility for TLH.

In the final step, we assess the two modes of TLH—direct indexing and index fund—by subtracting the TLH alpha with the index portfolio from the TLH alpha with direct indexing.

Index Descriptions:

Axioma 400 Index: The Axioma 400 Index is a capitalization-weighted portfolio composed of the 400 largest U.S. securities, representing large-cap equity performance across major sectors of the U.S. market.

S&P 500 Index: The S&P 500 Index measures the performance of 500 leading large-capitalization U.S. companies and is widely regarded as a benchmark for the overall U.S. equity market.

This material does not constitute investment advice and should not be viewed as a current or past recommendation or a solicitation of an offer to buy or sell any securities or to adopt any investment strategy. Harbor Capital and its associates do not provide legal or tax advice.

Any tax related discussion contained in this material, including any attachments/links, is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding any tax penalties or (ii) promoting, marketing, or recommending to any other party any transaction or matter addressed herein. Please consult your independent legal counsel and/or tax professional regarding any legal or tax issues raised in this material.

Tax-loss harvesting may not be appropriate for all investors and may not always result in reduced taxes. The strategy’s benefits depend on individual tax circumstances, market conditions, and future gains. Investors should consult a tax professional before making any investment or tax decisions.

Tax alpha refers to the portion of investment return generated through tax-efficient management rather than market performance. It represents potential after-tax benefits from strategies such as tax-loss harvesting.

The wash sale rule may limit or defer the tax benefits of realized losses if the same or a substantially identical security is purchased within 30 days before or after a sale. Investors should review their trading activity and consult a tax professional to understand how the rule may apply to their specific situation.

Quorus Inc. is not affiliated with Harbor Capital Advisors, Inc.

Copyright © 2025 Quorus Inc. All rights reserved.

.webp)